RY 144.17 0.4529% TD 77.39 0.0517% SHOP 78.87 -1.3878% CNR 171.64 0.5625% ENB 50.09 -0.4769% CP 110.62 0.6277% BMO 128.85 -0.548% TRI 233.58 1.1563% CNQ 103.29 -0.174% BN 60.87 -0.2295% ATD 75.6 -1.447% CSU 3697.0 1.1582% BNS 65.76 -0.3485% CM 66.6 -0.5525% SU 54.21 1.1569% TRP 53.15 0.3398% NGT 58.54 -0.3405% WCN 226.5 0.4123% MFC 35.905 0.9986% BCE 46.75 -0.5954%

Company Overview: Amdocs Limited is a provider of software and services for communications, entertainment and media industry service providers. The Company develops, implements and manages software and services associated with business support systems (BSS), operational support systems (OSS) and network operations to enable service providers to introduce new products and services, process orders, monetize data, support new business models and enhance their understanding of their customers. The Company's segment provides software products and services. Its services include strategic business consulting, systems integration and transformation, managed services and testing. Its managed services provide multi-year, flexible and tailored business processes and applications services, including application development and maintenance, information technology (IT) and infrastructure services, testing and professional services.

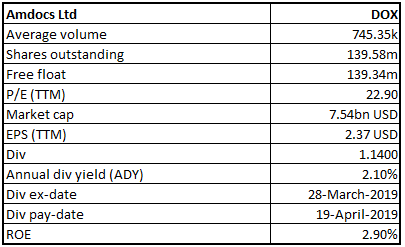

DOX Details

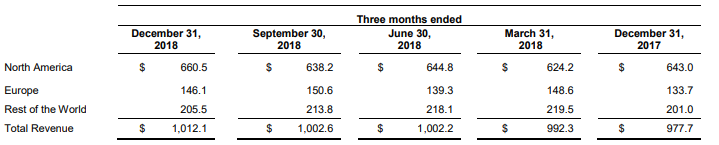

Mixed Performance for the first quarter of FY19: Amdocs Limited (NASDAQ: DOX) is a leading provider of software and services pertaining to the industry like communications, Pay TV and media all over the world. The company has strong long-term business relationships with more than 350 communications and media providers and has tie-ups with about 600 content creators for the technology and distribution. Recently, the company reported its Q1 FY19 results, wherein the adjusted earnings per share came in at 98 cents per share, which is broadly in-line with the market consensus’ estimates for the adjusted earnings per share of 99 cents per share. Q1 FY19 was mainly driven by winning several new deals, extending penetration into new regions and new customer gains over the period. The company reported a revenue growth of 3.5% to $1.012 billion in the first quarter of FY19, beating the markets’ estimates for the revenue of $1.007 billion. The company has posted the revenue for the first quarter of FY19, above the midpoint of $990 million to $1,030 million guidance range, which includes the negative impact from the movement of the foreign currency of about $4 million compared to the fourth quarter of FY18, and also compared to the company’s guidance for the first quarter of 2019. The company reported the non-GAAP operating margin of 17.3% for the first quarter of FY19, which reflects an expansion of about 10 basis points compared to the prior quarter (Q4 FY18) and is close to the higher end of the company’s long-term target range of between 16.5% and 17.5%. In Q1 FY19, the company posted the free cash flow (FCF) of $72.37 million, comprising of cash from operations of $109.65 million, from which, the net CapEx of amount $37.27 million has been deducted. DOX for the first quarter of FY19 posted the normalized free cash flow of $136.05 million, which has increased compared to $125.64 million posted a year ago. However, in the normalized free cash flow, the company has excluded the one-time cash payment of $55 million, which the company paid for the legal dispute settlement and noted as expense in the prior quarter. The normalized free cash flow excludes the payments for business realignment in FY18, which is a nonrecurring charge of $7 million and excludes about $2 million related to the development of the new campus in Israel, that is going for more than one year. At the end of the first quarter of FY19, the company reported a cash balance of approximately $458.65 million. Furthermore, the group recorded revenue growth at CAGR of 3.5% over the six years (FY13-18) and targeted the revenue growth of 0.5% to 4.5% year-over-year on a reported basis in FY19. Hence, we trust on the management’s ability to tap growth opportunities on the back of its business strategy supported by expanding its global client base by signing long-term contracts and synergistic acquisitions with major telecom industry players across the globe.

Revenue and Operating Margin Trend (Source: Company Reports)

Geographic Performance for the first quarter of FY 19: During the first quarter of FY19, for North America, the company reported revenue of $660.5 million, an increase of 2.7% on the back of requirements of Amdocs’ communications for digital modernization, Pay TV and media clients. During Q1 FY19, for Digital Pay TV, the group inked a multi-year contract to increase the Altice USA digital and mobile offering as part of its service strategy. The company’s outlook for North America remained strong driven by healthy activity levels in the region. At AT&T, the company has a healthy relationship with regard to offering services to underpin AT&T digital, network, media and services requirement. Further, the company has a healthy relationship with both T-Mobile and Sprint, which is undergoing consolidation. The consolidation activity can create temporary uncertainty in the near-term, and the company is unable to predict the outcome of this consolidation currently. Moreover, during the first quarter of FY19, for Europe, the company reported a 9.3% growth in the revenue to $146.1 million. The company, over the last few years, has invested organically into the acquisition for building the customer and service infrastructure in the key European markets. DOX has bagged significant projects with Italy's three largest service providers as compared to three years ago. The company has been successful in other parts of the European region, such as Ireland, Netherland and Spain, where the company has bagged significant projects. Further, the PJSC VimpelCom that operates under the Beeline brand in Russia has chosen DOX for a significant digital monetization project, including a multi-year Managed Services agreement. A Tier-1 service provider in Spain has signed the deal with Amdocs for a digital managed transformation. These contracts will offer positive multi-year growth outlook in Europe. Meanwhile, during the first quarter of FY19, for Rest of the World (ROW), the company’s first quarter revenue has fallen sequentially due to the normal fluctuation in customer project activity. The company for ROW during the first quarter of FY19 reported a 2.2% rise in the revenues to $205.5 million. During Q1 FY19, the company secured a new win in Pay TV media, where it has signed a five-year digital transformation deal with the leading content and consumer company in Southeast Asia. This move will significantly enhance both the media momentum and the cloud capabilities of the company. Rest of the World (ROW) also provides significant growth opportunities in the network domain, where the Globe Telecom in the Philippines has selected the company’s Network Functions Virtualization solution to automate the operation and management of its Network-as-a-Service offering for the enterprise customer. This is a landmark transformation deal for the company and includes the services agreement for five years.

Geographical Break-up of Quarterly Revenue (Source: Company Reports)

Backlog Increased for the Quarter: The company reported a backlog of $3.37 billion for the 12 months at the end of the first quarter of FY19, which is up by $10 million from the end of the prior quarter. The backlog includes the expected revenue that the company will receive from its contracts, estimated revenue due to managed services contracts, letters of intent, which the company holds, and maintenance and estimated revenue from the ongoing support activities. We presume that the company will continue to maintain its backlog and its executions, which can support top line growth in the future.

12-month backlog (Source: Company Reports)

Capital Management: DOX as per the Quarterly Cash Dividend Program declared a quarterly cash dividend of $0.285 per share. The company will pay this dividend on April 19, 2019, to the shareholders of record on March 29, 2019. Further, during the first quarter of FY19, the company repurchased $99 million of ordinary shares.

Outlook for FY19: For the second quarter of FY19, the company expects the revenues to be in the range of approximately $995 million to $1,035 million. The non-GAAP diluted earnings per share is expected to be in the range of approximately $1.00 to $1.06. For FY19, the company projects the revenue growth to be in the range of 0.5% to 4.5% year-over-year on a reported basis, which is lower than the previously guided range of 1.0% to 5.0%. The company reiterated the previous guidance for the revenue growth to be in the range of 2.0% to 6.0% year-over-year on a constant currency basis. The company has incorporated, in the fiscal 2019 revenue guidance, the anticipated negative impact that will arise due to the fluctuations of the foreign currency, which is estimated to be about 1.5% year-over-year as compared to a negative impact of approximately 1.0% previously. Further, the company also reiterated the guidance for non-GAAP diluted earnings per share growth for FY19, which is expected to be approximately 3.0% to 7.0% year-over-year.

Financial Ratios (Source: Company Reports and Thomson Reuters)

Stock Recommendation: DOX stock is trading at a price of $54.28, with support at $53.5 level and resistance at $60.7. The company is currently trading near its 52-week low level, but taking a closer look at its backlog, the company has a great potential to move upwards. The company is optimistic about the 12-month backlog that, at the end of first quarter FY19, reached $3.37 billion, which is up $10 million on a Y-o-Y basis. The company posted mixed performance during the first quarter of FY19. The company during FY18 reported double-digit growth in Europe and continues to receive significant projects in the region. The company has posted healthy growth in North America and the Asia Pacific during the quarter. On the analysis front, the stock is currently trading at lower EV/Sales and P/BV multiples of 1.8x and 2.2x as compared to the industry median of 4.3x and 2.8x, respectively, which keeps the stock in the attractive zone. Hence considering the aforesaid facts and current trading level, we give a “Buy” recommendation on the stock at the current market price of $54.28.

DOX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

CA

CA  AU

AU UK

UK US

US NZ

NZ Please wait processing your request...

Please wait processing your request...