RY 144.17 0.4529% TD 77.39 0.0517% SHOP 78.87 -1.3878% CNR 171.64 0.5625% ENB 50.09 -0.4769% CP 110.62 0.6277% BMO 128.85 -0.548% TRI 233.58 1.1563% CNQ 103.29 -0.174% BN 60.87 -0.2295% ATD 75.6 -1.447% CSU 3697.0 1.1582% BNS 65.76 -0.3485% CM 66.6 -0.5525% SU 54.21 1.1569% TRP 53.15 0.3398% NGT 58.54 -0.3405% WCN 226.5 0.4123% MFC 35.905 0.9986% BCE 46.75 -0.5954%

Company Overview: Bank of America Corporation is a bank holding company and a financial holding company. The Company is a financial institution, serving individual consumers and others with a range of banking, investing, asset management and other financial and risk management products and services. The Company, through its banking and various non-bank subsidiaries, throughout the United States and in international markets, provides a range of banking and non-bank financial services and products through four business segments: Consumer Banking, which comprises Deposits and Consumer Lending; Global Wealth & Investment Management, which consists of two primary businesses: Merrill Lynch Global Wealth Management and U.S. Trust, Bank of America Private Wealth Management; Global Banking, which provides a range of lending-related products and services; Global Markets, which offers sales and trading services, and All Other, which consists of equity investments, residual expense allocations and other.

.png)

BAC Details

Bank of America Corp (NYSE: BAC), which has a significant market capitalization, is a US based multinational investment bank and financial services company. The group has last month reported a strong 4Q18 result and group’s net income of $7.3 billion on net revenues of $22.7 billion was the key highlight. The result found support from strength in consumer base, wealth, and global banking businesses while BAC maintained healthy operating leverage and asset quality. The balance sheet has remained resilient given the CET1 ratio of 11.6%. Based on the performance trend, we expect BAC to demonstrate long-term potential while upcoming dividend payment and stability compared to peers give an edge to the bank and are certain attributes that look attractive in view of the latest result. Group’s 16 consecutive quarters of positive operating leverage, growth in EPS and a 16.3% return on average tangible common shareholders’ equity, set the base right for 2019.

.png)

Full year Performance (Source: Company Reports)

Strong Performance in the Fourth Quarter 2018: BAC in the fourth quarter of FY 18 has reported 49 percent growth in the adjusted earnings per share to 70 cents, which has beaten the average analysts’ estimates for the adjusted earnings per share of 63 cents. The company had reported 11 percent rise in the adjusted revenue growth to $22.7 billion in the fourth quarter of FY 18 underpinned by net interest income (NII), that reflects the benefits due to higher interest rates along with loan and deposit growth. The company has delivered 208% growth or growth of 39% after adjusting the impact of the Tax Act in 2017, in the net income to $7.3 billion on the back of continued strong 7% operating leverage, asset quality and the benefit of tax reform that has affected the 2018. The pretax income during the fourth quarter 2018 increased by 41% or 22% on an adjusted basis to $8.7 billion.

During the fourth quarter 2018, there has been 4% growth in the average deposits to $1.3 trillion year over year. There was a 3% growth in consumer banking deposits to $687 billion and this was owing to non-interest-bearing and low-interest checking that contributed to over half of Consumer Banking's deposits. On the other hand, the aggregate of money market accounts, CDs and savings, remained the same as prior corresponding period. There was a 3% growth in terms of deposits for Global Wealth and Investment Management (GWIM) on year over year basis. With the shift in trend from investments to cash, growth in GWIM's deposit balances was noted amidst the market volatility as consumers resorted to alternates. Global banking deposits grew by 9% year over year, on the back of the investments the company had made in client-facing bankers and global treasury services capabilities. There has been rotation from non-interest-bearing to interest-bearing deposits as expected in global banking. During the quarter, total loans on an average basis were $934 billion; however, run-off and sales of non-core consumer real estate loans impacted the total loan growth. By the end of the fourth quarter 2018 and similar to last quarter, the company has sold mostly non-core consumer real estate loans that have a book value of $5 billion, and posted a small profit.

Growth in consumer and commercial loans: A 4% growth in the consumer loans on a year over year basis, was reported given the mortgage and consumer credit card scenario. There has been 2% growth in the Commercial loans year over year. Additionally, during the fourth quarter of 2018, the company had posted the net interest income on a GAAP non-FTE of $12.3 billion, or $12.5 billion on an FTE basis. There has been 7% rise in the GAAP NII compared to the fourth quarter of 2017. Primarily, value over deposits with rise in interest rates and the loan and deposit growth positively attributed to the overall scenario while higher funding costs in global markets and lower loan spreads acted as negative factors. On a sequential basis, the GAAP NII grew by $434 million. September rate hike, loan and deposit growth, and lower long-term debt expense helped the sequential quarter growth. Net interest yield during the fourth quarter of 2018 had improved 9 basis points to 2.48% year over year. On the other hand, lower-yielding global market assets impacted the otherwise decent improvement in the core banking activities.

.png)

Fourth Quarter 2018 Financial Performance (Source: Company Reports)

Strong Credit Quality: During the fourth quarter of 2018, BAC’s overall credit quality continued to remain strong across the company’s consumer and commercial portfolios. There was fall of $313 million in the net charge-offs to $924 million. This was on the back of the absence of the prior year's single-name non-U.S. commercial charge-off. There was a decline of 14 bps in the net charge-off ratio to 0.39%. There has been a fall of $96 million in the provision for credit losses in the fourth quarter 2018 to about $905 million. In the Q4 2018, the provision expense increased by $0.2B from 3Q18 to $0.9B, and this closely matched with the net charge-offs. Moreover, during the fourth quarter 2018, there has been a fall in the nonperforming assets by $1.5 billion to $5.2 billion, underpinned due to the improvements in consumer. Further, there has been a fall of 18% in commercial reservable criticized utilized exposure to $11.1 billion, which is on the back of broad-based improvements across several industries.

.png)

Asset Quality (Source: Company Reports)

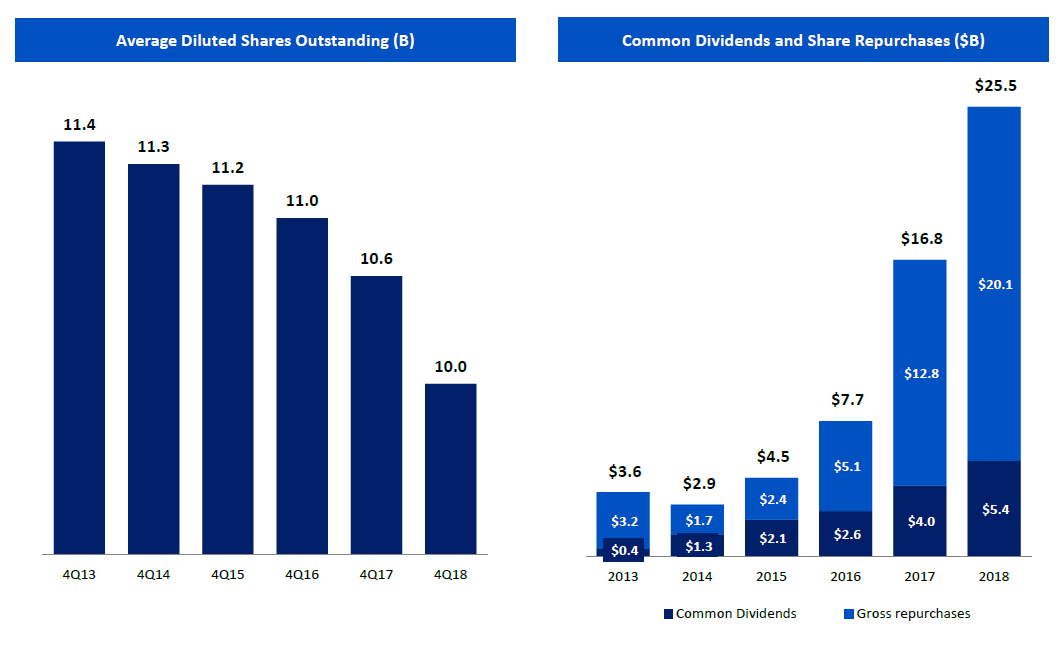

Dividends and Capital Management: During 2018, BAC had repurchased $20.1 billion in common stock and had paid $5.4 billion as dividends. A quarterly cash dividend for the BAC stock of $0.15 per share, has been declared by the bank and this is to be paid on March 29, 2019 to shareholders of record as at March 01, 2019. Further, a regular quarterly cash dividend of $1.75 per share has been declared on the 7% Cumulative Redeemable Preferred Stock - Series B; and this will be payable on April 25, 2019 to shareholders of record as at April 11, 2019. Moreover, BAC has increased its common stock repurchase program by an additional $2.5 billion to $22.5 billion, which has to be repurchased by June 30, 2019. Previously, the company had announced the repurchase plans on June 28th, 2018 to repurchase about $20.0 billion from July 1, 2018 through June 30, 2019. These repurchases have been indicated to offset shares awarded under equity based compensation plans during the same period, and have been said to be amounting to about $ 0.6 billion. The company has approved the additional repurchases, which in total will offset an expansion in regulatory capital that rose due to the sale of some non-core assets in 2018. The Federal Reserve Board has already approved these additional repurchases. On the other hand, BAC’s liquidity continued to remain strong during the fourth quarter 2018, the average global liquidity sources were of $544 billion, and all the company’s liquidity metrics was well above the company’s requirements. There was a decline of $5 billion in the long-term debt and maturities had outpaced the issuances. BAC is in compliance with the TLAC rules comfortably that had become effective in January, particularly due to the recent reduction in the Method 1 GSIB. The company expects that the parent debt issuances in 2019 would be less than their maturities. Additionally, during the fourth quarter 2018, there has been rise in the total shareholder equity by $3 billion compared to the third quarter 2018, as the accumulated other comprehensive income (AOCI) benefited due to the rise in the value of the AFS debt securities. There has been 22 basis points' improvement in CET1 standardized ratio to 11.6% from the third quarter as it continued to remain above the requirement of 9.5%. The improvement was on the back of the increase in AOCI along with the slight decline in RWA (risk-weighted assets). Softness in lower global markets' RWA was the key reason for the above while sale of non-core consumer loans also played a role. These factors together offset the impact of loan growth across BAC businesses.

Capital Returned to Shareholders (Source: Company Reports)

Future Outlook: The Federal Reserve's projection shows that there might only be one more rate hike this year, that too if required and this may still help the bank though chances of a dovish tone may be higher. For FY 19, BAC expects that the expenses would approximately be at the level of 2018. The 2019 expenses will include the expenditure of approximately $1 billion planned for normal yearly merit, healthcare benefits, inflation, marketing, new investments in technology along with the expansion and modernization of financial centers. However, for the first quarter of 2019, the expenses would rise compared to the fourth quarter of 2018 by approximately $500 million on the back of seasonal personnel costs, which will be mostly payroll tax. The company estimates that the expenses would gradually be moving to a lower side from the first quarter through the remaining quarters of 2019.

Stock Recommendation: BAC stock is trading at a price of $28.7, and has support at $23.4 level and resistance around $31. BAC has posted better than expected earnings for the fourth quarter of 2018. The fourth quarter results were underpinned by four interest rate hikes by the central bank in 2018, and on the back of a strong job market that kept bad loans in check and borrowing decent. Fundamentally, the group’s net interest margin has enhanced from 2.42% of September quarter to 2.48% in December and loan growth has been up drastically. The pre-tax ROE has moved up to 13% in 2018 and this is over the industry margin of 12.4%. Considering the Forward 24 months EPS of over $3, a low double digit rise in stock price is expected. Given the above backdrop, we have a “Buy” recommendation on the stock at the current price of $ 28.7.

.png)

BAC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

CA

CA  AU

AU UK

UK US

US NZ

NZ Please wait processing your request...

Please wait processing your request...