RY 144.17 0.4529% TD 77.39 0.0517% SHOP 78.87 -1.3878% CNR 171.64 0.5625% ENB 50.09 -0.4769% CP 110.62 0.6277% BMO 128.85 -0.548% TRI 233.58 1.1563% CNQ 103.29 -0.174% BN 60.87 -0.2295% ATD 75.6 -1.447% CSU 3697.0 1.1582% BNS 65.76 -0.3485% CM 66.6 -0.5525% SU 54.21 1.1569% TRP 53.15 0.3398% NGT 58.54 -0.3405% WCN 226.5 0.4123% MFC 35.905 0.9986% BCE 46.75 -0.5954%

Company Overview: Merck & Co., Inc. is a global healthcare company. The Company offers health solutions through its prescription medicines, vaccines, biologic therapies and animal health products. It operates through four segments: Pharmaceutical, Animal Health, Healthcare Services and Alliances. The Company's Pharmaceutical segment includes human health pharmaceutical and vaccine products marketed either directly by the Company or through joint ventures. Human health pharmaceutical products consist of therapeutic and preventive agents, generally sold by prescription, for the treatment of human disorders. The Company sells its human health pharmaceutical products primarily to drug wholesalers and retailers, hospitals, government agencies and managed healthcare providers, such as health maintenance organizations, pharmacy benefit managers and other institutions. Vaccine products consist of preventive pediatric, adolescent and adult vaccines, primarily administered at physician offices.

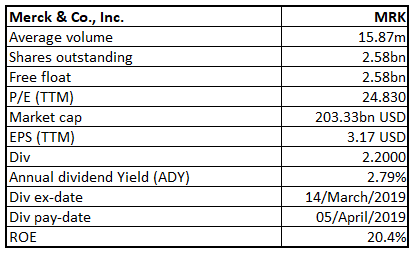

MRK Details (ROE as at 2018)

Strong Performance in the first quarter of FY19: Merck & Co., Inc. (NYSE: MRK), the US based pharma company, that has market capitalization of ~$203.3 billion (as on 01 May 2019) has posted better than expected results for the first quarter of FY19. The company has raised the forecast for the FY19. The company performed well on the back of strong performance witnessed by oncology, vaccines, and select hospitals and specialty products. MRK’s international business, that forms 58% of the sales in the first quarter of 2019, has witnessed strong momentum during the quarter. MRK in the first quarter of FY19 has reported the adjusted EPS (Earnings Per Share) of $1.22, higher than EPS of $1.05 in 1Q FY18. The company had reported the adjusted revenue growth of 8% to $10.82 billion in the first quarter of FY19. The company has improved its non-GAAP gross margin to 75.9% in the first quarter of FY 19 from 75.7% in 1Q FY18. The improvement in non-GAAP gross margin is on the back of the positive effects of foreign exchange movement and efficient product mix, which was partially offset due to the rise in amortization of intangible assets that is related to collaborations and also due to the negative effects of pricing pressure and royalties. The company has posted 3% decline in the Non-GAAP selling, general and administrative expenses to $2.4 billion in the first quarter of 2019, compared to the first quarter of 2018. This decline in the expenses is due to low cost of promotion and selling and the positive effects of foreign currency movements, which was partially offset due to high administrative costs. The company has witnessed 9% rise in the Non-GAAP R&D expenses to $2 billion in the first quarter of FY19 compared to the first quarter of FY18. The R&D expenses rose due to rise in clinical development that includes the collaborations and investment in the development of early drug. Overall, the net income of the company has approximately quadrupled to $2.92 billion during the first quarter of FY19 from $736 million posted in the corresponding quarter a year earlier. This is on the back of the $1.4 billion charge that the company had taken due to a collaboration deal with Japanese drug-maker Eisai Co Ltd. Further, MRK has planned a restructuring program for the optimization of its manufacturing and supply network and to reduce its real estate footprint and it is expected that the company will post the charges related to restructuring cost of $500 million in FY19.

Segment Performance during the First Quarter of FY19: Revenue from pharmaceutical segment grew 8% to $9.7 billion during the first quarter of FY19 compared to the first quarter of FY 18. This segment grew on the back of the growth in oncology and vaccines, which was partially offset due to the effects of the loss of market exclusivity on several products like ZETIA (ezetimibe) and VYTORIN (ezetimibe/simvastatin), medicines to lower the LDL cholesterol, INVANZ (ertapenem sodium), an antibiotic, CANCIDAS (caspofungin acetate), an antifungal, and REMICADE (infliximab), a treatment meant for treating inflammatory diseases. The growth in oncology was due to 55% increase in sales of KEYTRUDA to $2.27 billion. Meanwhile, Keytruda has received the European approval for the first-line treatment of metastatic squamous NSCLC. The European Commission had approved 45 days dosing schedule throughout all current monotherapy indications for KEYTRUDA. The growth in sales of oncology was on the back of $79 million from alliance revenue related to Lynparza and $74 million with respect to Lenvima. Further, a rise in sales of the vaccines was witnessed because of a rise in the sales of GARDASIL and GARDASIL 9 vaccines which are meant to inhibit certain cancers as well as other diseases which are caused by Human Papillomavirus (or HPV), mainly driven by the ongoing commercial launch in China. The company has posted 27% rise in Gardasil sales to $838 million.

Also, the sales of vaccines witnessed the rise because of increased demand in Europe, which is largely driven on the back of a rise in the rates of vaccination meant for both boys and girls, coupled with the timing of customer purchases in Latin America. This growth, however, was partially offset due to the decline in sales in the United States. The sales growth in pediatric vaccines was on the back of the VARIVAX (Varicella Virus Vaccine Live), which is a vaccine meant to prevent chickenpox, PROQUAD (Measles, Mumps, Rubella and Varicella Virus Vaccine Live), which is a combination and M-M-R II (Measles, Mumps and Rubella Virus Vaccine Live). These drugs encountered the rise of 27% and stood at $496 million due to government tenders in Latin America as well as a rise in the demand in Europe and the US. Currently, the measles cases in the United States are at their highest level from the time the virus was declared eradicated in 2000, and has increased over a period of time, signifying an opportunity for MRK being a sole provider of the measles-mumps-rubella vaccine. Moreover, during the first quarter of 2019, the company has reported 4% decline in the sales from Animal Health segment to $1 billion compared to the first quarter of FY18. However, excluding an unfavorable effect which was witnessed in foreign exchange, the sales from Animal Health segment increased 3% in 1Q FY19. This sales growth was because of a rise in demand for the companion animal products, primarily the BRAVECTO (fluralaner) type of products which are meant to control parasites as well as a rise in the volume of livestock products. The company had reported the profits amounting to $415 million from Animal Health segment in Q1 FY 2019, which is almost flat as compared to $413 million in the Q1 FY 2018. In the month of April 2019, the company had made the acquisition of Antelliq Group, which happens to be a leader when it comes to digital animal identification, traceability and monitoring solutions.

Revenue Performance for the First Quarter of FY 19 (Source: Company Reports)

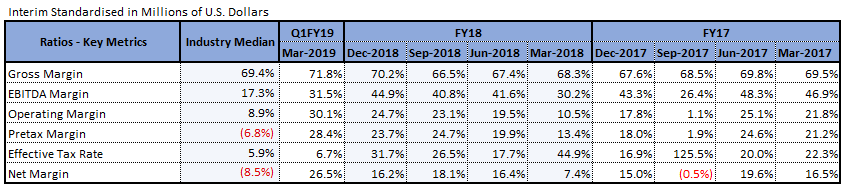

Other Highlights: MRK received FDA acceptance for priority review for ZERBAXA for the treatment of adult patients suffering from nosocomial pneumonia and ventilator-associated pneumonia, investigational beta-lactamase inhibitor relebactam in combination with imipenem/cilastatin to treat certain infections triggered by certain susceptible Gram-negative bacteria. The company extended research phase tie-up for the span of next 3 years with NGM Biopharmaceuticals and has its focus to discover, develop as well as commercialize the novel biologic therapeutics throughout the range of therapeutic areas. Its EBITDA margin and net Margin for H1FY19 stands at 31.5% and 26.5% better than the industry median of 17.3% and -8.5% respectively.

Key Ratio Metrics (Source: Thomson Reuters)

Outlook for FY19: The company has raised the EPS forecast for the full-year 2019, and expects it to be in the range of $4.02 to $4.14 and the 2019 adjusted earnings per share to be in the range of $4.67 to $4.79. The new range reflects a growth of about 8% to 10% compared to FY18. MRK expects the revenue to be in the range of $43.9 billion to $45.1 billion reflecting a growth of 4% to 7% as compared to FY18, which is projected on the back of the strong growth across the oncology, vaccines, hospital and specialty and Animal Health businesses. The company projects FY19 Non-GAAP operating expenses to be higher than FY18 and expects it to be low to mid-single digit rise. Non-GAAP tax rate for FY19 is expected to be in the range of 18.5%-19.5%.

2019 Financial Guidance (Source: Company Reports)

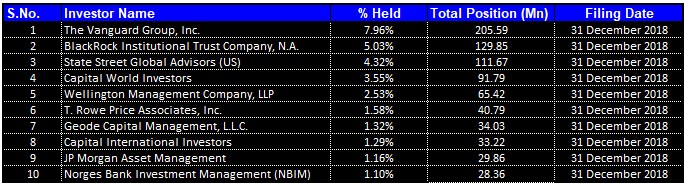

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form 29.83% of the total shareholding. The Vanguard Group, Inc and BlackRock Institutional Trust Company, N.A. hold maximum interest in the company with a stake of 7.96% and 5.03% respectively.

Top Shareholders (Source: Thomson Reuters)

Stock Recommendation: The company has recorded excellent results in the first quarter of FY19 and has raised the outlook for FY19 for both top-line & bottom-line. Strong demand for KEYTRUDA & GARDASIL and other products, monopoly of PROQUAD vaccine, acquisition to strengthen its animal health revenue segment along with good fundamentals augur well for the prospects of the business. Its EBITDA margin and net Margin for H1FY19 stands at 31.5% and 26.5% better than the industry median of 17.3% and -8.5% respectively. Currently, the stock is trading at $78.72, has support at $72.25 level and resistance at $84. MRK is well positioned to address the unmet medical needs with its current product portfolio, strong product-pipeline with higher on research and development. Considering the above-mentioned positives, we give a “buy” recommendation on the stock at the current market price of $78.72, considering an expectation of a single-digit upside in the next 12-24 months.

.png)

MRK Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Canada Advisory Services Inc. and provided on this website is general information only and it does not take into account your investment objectives, financial situation and the particular needs of any particular person. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. The website www.kalkine.ca is published by Kalkine Canada Advisory Services Inc. The link to our Terms & Conditions has been provided please go through them. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

CA

CA  AU

AU UK

UK US

US NZ

NZ Please wait processing your request...

Please wait processing your request...